LISTEN TO THIS ARTICLE:

The Bank of Japan (BOJ), Japan’s central bank, is currently known as one of the most innovative central banks in the world. Unlike other major central banks, the BOJ has faced economic conditions not seen in other parts of the world for the last couple of decades.

Forced to fight deflation when no other developed country was facing such conditions, the BOJ had to innovate and come up with solutions often thought of as radical by the rest of the world. Yet, time has proved that what the BOJ did was only the start of an unconventional monetary policy. Faced with similar problems over the years, the world quickly learned from the BOJ’s actions and adapted them to the local conditions.

The BOJ plays an active role in the value of the local currency, the Japanese yen (JPY). Because Japan is the world’s third-largest economy (behind the United States and China), the strength of the local currency has a major influence on the international financial markets. Moreover, the JPY was and still is the primary currency responsible for the risk-on and risk-off moves in the United States and the global stock markets – a point we will discuss later in this article.

As is very often the case, the BOJ maintains close ties with major central banks around the world. Representatives of those banks have visited Japan numerous times to advise on economic and monetary policy decisions that suit the country best. However, this occurs not just with the BOJ but with all major central banks; cooperation under the Bank for International Settlement (BIS) umbrella is the new normal.

An aging demographic brought changes in Japanese spending habits, causing major shifts in monetary policy and a deflationary wave that was difficult to combat.

Bank of Japan’s History

Established in 1882, the BOJ is one of the oldest central banks in the world. The bank was fully reorganized in 1942 and 1949 as a consequence of World War II. As the Japanese economy shifted from closed to open, the BOJ moved its focus from a fixed currency exchange rate to a variable exchange rate.

Throughout major economic events in history, the BOJ has acted swiftly to maintain price stability and a competitive JPY on the international markets. For instance, in August 1971, when the Nixon shock occurred (the United States ended the USD convertibility to gold), the BOJ kept the fixed exchange rate it was pursuing at that time. The idea was to create excess liquidity and then raise the official bank rate to curb skyrocketing prices. The experiment succeeded.

Another example of the swift way the BOJ operates comes from 1985. The Plaza Accord weakened the USD significantly, including against the JPY. As a consequence, the BOJ began cutting interest rates, and, from that moment on, it kept on cutting them. However, there was little or no effect on the JPY as the currency became stronger and stronger.

In 1995, deflation gripped the Japanese economy. Deflation is an economic phenomenon in which inflation turns negative. It creates a number of problems because one of the major consequences is that consumers will postpone spending, usually for a long period of time.

From that moment on, deflation was the BOJ’s main problem. Despite tremendous efforts (e.g., qualitative and quantitative easing), the BOJ had a difficult time bringing inflation back to target. Speaking of target, like other central banks around the world, in 2013 the BOJ introduced a 2% inflation target, or price stability target, in terms of the YoY rate of change in the CPI.

Organization of the Bank

The BOJ has a Policy Board composed of nine members – one governor, two deputy governors, and six regular members. The Policy Board is the highest decision-making body and determines the guidelines for carrying out the bank’s operations. The governor represents the BOJ and oversees the control of its business, while the two deputy governors assist the governor in the day-to-day operations.

Besides the governor and the two deputy governors, there are six executive directors. Together with the deputy governors, they run the Management Committee and the Compliance Committee. The first committee manages issues regarding the bank’s operations, while the second one makes sure that officers and employees perform their duties in compliance with the bank’s rules.

The BOJ has no less than thirty-two branches that conduct operations such as currency issues or economic research in their areas. In addition to the branches, fourteen local offices also exist to help with the branches’ activities. Finally, the BOJ has seven overseas representative offices that gather information and conduct research as well.

In some parts of the world, the government charges central banks with supervising the banking system, but in Japan this role is assumed by a different authority that acts as a banking supervisor – the Financial Services Agency (FSA).

Monetary Policy in Japan

The process through which a central bank influences the quantity of money in an economy is called monetary policy. Money and money creation have always had a mysterious aura for the general public, but in reality, the process is simple and easy to understand.

A central bank like the BOJ monitors economic developments in the country, but also other factors with the potential to influence future economic performance (e.g., demographics). Based on the outcomes provided by the research department, the BOJ sets the monetary policy for the period ahead.

This process is valid not only for the BOJ, but also for most central banks in the developed world. Moreover, central banks in developing countries implement a similar process.

Effectively, central banks, including the BOJ, deal with controlling and monitoring the quantity of money and its velocity, by looking at things like the demand for money in the economy. It can control this demand via the main interest rate by stimulating central banks to loan money to people and businesses in the real economy (thus expanding the money base) or to be reluctant to do that (thus contracting the money base). Such monetary policy has a bearish effect on the local currency in the first case and a bullish one in the second case.

But in today’s complex financial world, things are not so easy. Yes, most of the time a currency reacts like this, but that is not always the case. The BOJ should know – it is a pioneer in Quantitative Easing (QE), a process via which the central bank buys its own government’s debt, designed to weaken the currency. Several years after the program’s inception, its success is still in question.

The BOJ’s Mandate

The pillar of the monetary policy is the central bank’s mandate. Effectively, it outlines what the central bank’s role is and what it is trying to accomplish.

21st-century central banking in the modern world centers on the monetary policy around inflation, but variations from country to country and region to region do exist. In some parts of the world, like the United States, the central bank’s mandate also involves job creation. Therefore, when setting the monetary policy, the United States Federal Reserve (the Fed) considers both inflation and job creation before setting the monetary policy.

Price stability is the main objective of monetary policy in Japan. Naturally, it relates to controlling inflation and bringing it to the desired target. Consensus has been built since the end of the 1980s that if the central banks adopt an inflation target, it would be easier to achieve the price stability mandate. However, as this article reveals later, the BOJ does not target a specific level for inflation.

Besides price stability, the BOJ manages the banknotes in circulation, provides settlement services, thus improving the financial system’s stability, and compiles data, research activities and economic activities.

The measures that the BOJ undertakes to fulfill its mandate are closely watched by traders around the world. The JPY is one of the most traded currencies in the world, after the USD and the EUR, and it has influenced FX flows over the last century.

After World War II, Japan did not spend much time in the rubble for long. The economy quickly rebounded, and the country became an economic success, a worldwide economic powerhouse with exports all over the world. The value of its currency, the JPY, played and still plays a crucial role for traders and investors alike.

Money Measures

Most modern authorities produce a series of money measures to better handle the money stock. Effectively, we talk not only about the currency in circulation, but also about all forms of money available in an economy.

The main distinction made is between narrow and broad money. The first category comprises notes and coins in circulation, but also other liquid deposits. On the other hand, broad money comprises everything that fits into the narrow money category plus anything that can be used to make purchases.

A central bank is charged with knowing all the time the level of money supply and, by using money measures, it has a better idea of how money in an economy fluctuates. Moreover, by monitoring money measures and the money supply in the economy, central banks supervise the monetary policy transmission mechanism – how long it takes for monetary policy decisions to make their way into the real economy and, ultimately, their effects.

The BOJ supervises three measures of money in Japan. The first one is the narrowest one, called M1, and it deals with the coins and cash in circulation. By adding certificates of deposit to M1, the BOJ monitors a second measure of money. Finally, the third measure also comprises deposits and other savings with financial institutions or commercial banks.

Establishing and Communicating the Monetary Policy in Japan

The BOJ follows a multi-step procedure for establishing and communicating the monetary policy in Japan. First, it holds a monetary policy meeting where it reviews past and current economic conditions and the forecast for the period ahead.

Next, it releases an outlook report, which is literally the bank’s view and its conclusions after the economic and monetary assessment. Moving forward, a Summary of Opinions follows, and finally, the monetary policy meeting minutes.

Every time the bank convenes (about eight times each year), the process is identical. However, the releases are scheduled at different dates and times between two monetary policy meetings, giving the financial world a second opportunity to understand the message if it did not do so in the first place.

Monetary Policy Meetings

As mentioned earlier, the BOJ’s ruling body meets every six weeks for its regular monetary policy meeting. At the end of the meeting, which does not have a scheduled time on economic calendars, the BOJ communicates its decisions by issuing a statement comprising the main decisions it took.

For instance, the statement may refer to the impact of the coronavirus health crisis on Japan’s economic performance, to JGBs (Japanese Government Bonds) and T-Bills (Treasury Bills) purchase activities, to the guidelines for market operations, or to possible changes to its Quantitative and Qualitative Easing (QQE) program.

As a side note, the BOJ is one of the most aggressive central banks when it comes to easing the monetary policy, and its programs far exceeded those in other parts of the world during the Great Financial Crisis in 2008. Since then, it has continued to ease the monetary policy via various tools, including buying Exchange Traded Funds (ETF) directly or using the yield curve control to achieve its mandate of keeping price stability around the 2% target level.

- What Traders Need to Know

News related to changes in any of the programs previously run by the BOJ or new ones recently introduced creates extreme volatility in the currency market. Moreover, because of the role the JPY plays for the other central banks (e.g., the Fed) and investors in the stock market, changes in the monetary policy in Japan have the power to move the entire financial system. For instance, the United States Fed runs the System Open Market Account (SOMA) program that is literally a large-scale asset purchase program. As part of this program, it buys not only USD-denominated assets but also JPY- and euro-denominated ones. Hence, changes in the monetary policy in both Japan and the Eurozone have a strong influence on monetary policy in the United States too.

The most important thing to remember about the BOJ monetary policy meetings is that there is no scheduled time when the monetary policy decision is released to the public. All traders and investors know is the day, but not the time. However, recent years have seen a more disciplined approach to the statement release, and market participants can anticipate, more or less, an approximate time during the trading day when to expect the statement.

The Bank’s View or the Outlook Report

On the same day the BOJ announces the monetary policy decision, it also releases the Outlook Report. While a snapshot is released immediately after the monetary policy meeting, the full report is available at 2:00 PM on the next business day.

This is an important piece of economic information about Japan as the report is comprehensive – usually exceeding tens of pages of economic data, statistics, research, and so on. Therefore, for investors interested in everything related to the Japanese economy, if there is one report to consider analyzing, this is the one.

It begins with a quick summary and then dives into economic details regarding financial conditions, the outlook for the economic activity and prices in Japan, forecast of the majority of the policy board members regarding the real GDP and Consumer Price Index (CPI), the external balance situation, corporate profits – a full and comprehensive analysis of everything happening in the Japanese economy in the previous six weeks and a forecast for the period ahead.

Because this snapshot is released right after the monetary policy meeting, the market does not react much to the Outlook Report release. However, for medium to long-term investors, which typically are fundamental investors looking for turning points in macroeconomic factors and in the local conditions that affect the business cycle, the report is a cornerstone to any investing decision in Japan or in the Japanese currency.

- Summary of Opinions

The monetary policy communication process continues with the Summary of Opinions. Released two weeks after the monetary policy meeting, it summarizes the views of the policy board members regarding economic and financial developments, prices, as well as opinions about the monetary policy stance. Moreover, the Ministry of Finance and the Cabinet Office, as the government representatives, will state their view too.

Traders and investors look for discrepancies between what the Outlook Report showed and the Summary of Opinions content. Because the latter is released two weeks after the former, it tends to have a muted effect on the financial markets and the JPY in particular.

- Monetary Policy Meeting Minutes

The process of communicating the monetary policy is not over yet. Its final step consists of the publication of the monetary policy meeting minutes.

Two months after the monetary policy meeting, the BOJ releases the minutes of that meeting. The statement comprises the staff reports on economic and financial developments, overseas economic developments that might affect the Japanese economy (e.g. the U.S.-China trade war), and so on. At the end of the monetary policy meeting minutes, investors can find the original statement from the meeting that took place the month before.

For traders analyzing the BOJ’s calendar for its monetary policy communication process, the minutes release is tricky. Because of the lag between the actual monetary policy meeting and the minutes’ release, many traders think that the minutes refer to the last monetary policy meeting. In fact, they refer to the meeting that took place two months earlier, and in the meantime, a new meeting may have taken place.

To avoid confusion, keep in mind the following order. First, the BOJ holds the monetary policy meeting every six weeks. On the same day, with the monetary policy statement, it releases the Outlook Report. Next, two weeks later, the Outlook Report is released to the public. Finally, the minutes are made public two months after the monetary policy meeting took place.

Interest Rate Decisions and Their Effect on the Currency Market

The BOJ has had a very expansionary monetary policy for quite some time. Interest rates were lower in Japan long before the 2008 Great Financial Crisis (GFC), as the aging population posed unexpected problems for the economy.

Older people tend to spend less and take fewer risks when it comes to running businesses or starting new economic ventures. The tendency, therefore, is to save for the next generation and to avoid spending.

The problem became more acute when the natality rate dropped significantly. The economic implications for an economy with an aging population and low migration have tremendous impact on the labor force, construction activity, and so on. Decreasing levels of consumer spending made it difficult for the Japanese economy to expand at the rates seen after the Second World War.

Soon, people began leaving their houses and moving to smaller apartments due to the fact that they had no one to leave their houses to. This created a vicious cycle for economic growth and the BOJ was forced to keep the interest rates as low as possible to reach the mandate of price stability. As a reminder, price stability refers to an inflation level below but close to 2%, not inflation levels close to zero.

Faced with such an unfavorable outlook, the BOJ did like any other modern central bank would do – it kept the policy expansionary. But this works in global economic upturns. After the peak of the business cycle, during economic recessions or contractions, central banks react by expanding the monetary policy via rate cuts, and so on. But the BOJ already did that during economic growth, so it was often caught on the wrong foot with little or no tools to fight economic downturns.

Inflation Targeting in Japan

Unlike any comparable central bank in the world, Japan does not officially target the 2% inflation rate. As mentioned earlier in this article and throughout this trading academy too, moderate inflation is viewed as one of the main factors that spur growth.

Contrary to popular belief, rapid economic growth is not something that a central bank wants to see. Nor does it want to see slow growth.

In the first case, the economy is said to overheat. This puts pressure on prices, workers fight for higher wages and, as a result, inflation rises too much, offsetting the economic growth. Therefore, the central banks monitor inflation and, if it is on a path to rise above the 2% level, they will try to curb it by hiking the interest rate. In other words, the monetary policy becomes contractionary as money becomes scarce.

On the other hand, negative economic growth or slow growth reduces the consumer confidence levels. If consumers do not spend, the economy cannot grow at a steady rate. Therefore, inflation expectations drop, affecting everyday prices. The central banks intervene at this time to expand the monetary base, by lowering the interest rate and adopting other easing monetary policy measures.

The BOJ has dropped the 2% inflation target rate for the simple reason that no one believes it anymore. Therefore, if the consumer does not believe in the 2% inflation target, inflation expectations will not reflect it. Hence, the target cannot become a self-fulfilling prophecy, as central bankers call it.

The chart below shows the inflation rate in Japan for the last twenty-five years. Only on three occasions did the BOJ manage to push inflation above the 2% target, and the most recent try was when it started an unprecedented program to use unconventional measures in order to ease further.

Deflation in Japan

The fact that the Bank of Japan did not manage to reach the 2% inflation target is only one part of the problem. The bigger issue comes from the fact that inflation dropped below the zero level for a long time, and is still threatening to move there, despite the BOJ’s efforts.

When inflation turns negative, it is said that the economy is gripped by deflation. This economic phenomenon is exceedingly difficult to combat with traditional monetary policy tools, especially if the central bank is already holding the interest rate at almost zero.

The above chart shows that even before the year 2000, Japan had deflationary years. Also, from 2000 to 2010, inflation turned positive only sporadically. It all culminated in a move below -2%, in the aftermath of the 2008 financial crisis.

The chart makes an important point – the BOJ had to use other measures in order to create inflation to reach the 2% (unofficial) target and, thus, to stimulate economic growth. How else was Japan to compete with the rest of the world that was not facing the devastating economic phenomenon of deflation?

Its solution was to engage in a QE program that dwarfed what the United States Fed was doing at that time. To fully understand the dimensions, imagine that the QE program in Japan was three times bigger than the one in the United States, applied to an economy almost two times smaller. As such, Japan became an “experiment” from a monetary policy point of view, and the rest of the world watched in awe for the outcome.

However, as of mid-2020, there is little or no sign that inflation will get close to the BOJ target. Therefore, the BOJ is forced to search for further ways to fulfill its mandate of price stability around the 2% inflation target.

The Zero Interest Rate Policy

The start of the zero interest rate policy in Japan can be dated back to 1999. However, after only one year, the BOJ was forced to give it up due to an unforeseen crisis – the dot com bubble in the United States. Nevertheless, towards the end of 2001, the BOJ embraced another innovative policy – it adopted the balance of the current account as its main operating target, distancing itself from the zero interest rate policy.

Also called the quantitative relaxation policy, the move had a positive effect on economic growth in Japan at that time. By 2006, Japan had finished the quantitative easing policy and the zero interest rate policy and raised the rates to 0.25%.

It is interesting to note here that global economic growth was at its highest at this time. Signs started to appear that signaled the peak of the business cycle in the United States and other developed economies, but worldwide growth was still robust. For this reason, many central banks raised their interest rate level accordingly, with Japan being forced to merely raise it above the zero level.

Because of “traditionally” lower interest rates in Japan, a new phenomenon appeared in financial markets, one that will mark the international flows for a long time: the carry trade and the risk-on/risk-off environment.

By the time the 2008 financial crisis hit the developed world hard, the Japanese economy had started to suffer again. While other central banks had the luxury of cutting the interest rates from much higher levels, the BOJ was already at its lower boundary (0.25%). As such, unprecedented times required unprecedented measures – so the BOJ began buying Japanese Government Bonds (JGBs).

The JPY and the Risk-On/Risk-Off Trades

The risk-on/risk-off trading environment was mentioned earlier in this article, and at this point there is enough information presented to explain what it is and why it was so important for so long. Effectively, investors around the world searched for the cheapest way to borrow capital for investing in the US stock market. Where do you think they found it? In Japan, of course.

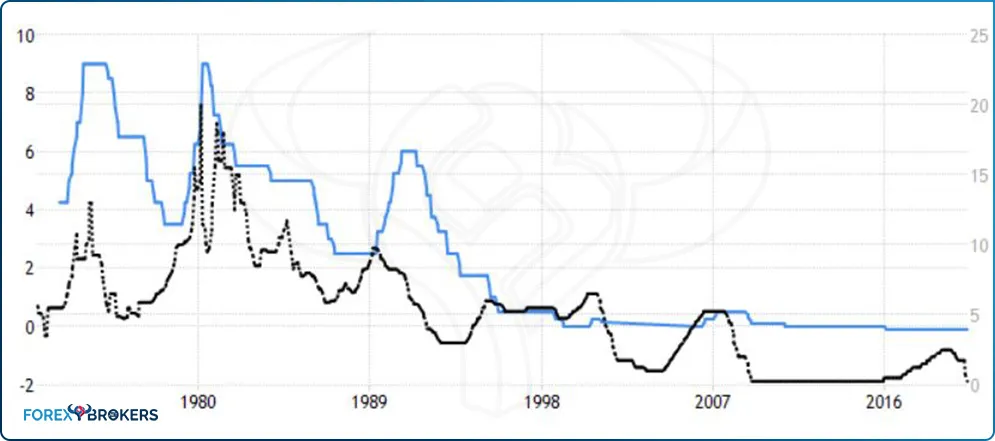

The blue and black lines on the chart above show the Japanese interest rate and the US federal funds rate, respectively, for the past fifty years. Focus on the vertical scales on the left and right side of the chart!

For anyone looking at this chart, the difference between the two monetary policies is obvious. While Japan kept the interest rate on the JPY close to zero or even below for more than twenty years, the federal funds in the United States were well in positive territory. Sometimes, the difference exceeded a full 5% – a staggering gap.

So, here is what investors did for years in order to buy US stocks. First, they borrowed capital in JPY, due to the lower borrowing costs. Next, they used JPY to buy USD. Finally, they used the proceeds to pay for the US stocks with USD.

In the market, the process translated into the following moves. First, the USDJPY pair moved higher, due to the selling of the JPY and buying of the USD. Second, the US stock market moved higher, reflecting investors’ desire to bid for equities. Finally, the entire situation described here created a risk-on environment (when investors buy stocks, it is said that they buy risk), sending EURUSD, GBPUSD, AUDUSD, NZDUSD higher, and USDCAD lower. The opposite happened when the investors pulled their investment from the stock market, creating a risk-off environment.

BOJ Interest Rate Evolution – A Historical Perspective

The struggles the BOJ has faced throughout time are obvious if we look at the interest rate from a historical perspective. They reflect the difficult task of setting the right monetary policy on an economy facing deflation and an aging population.

The thing is that the BOJ applied the same standard measures and tools as other central banks in the world did when their economies contracted or when inflation fell. In fact, seeing little or no success at the end of its operations, the BOJ innovated, becoming a leader in unconventional monetary policy.

The last time interest rates in Japan were above 2% was at the start of the 1990s. Since the beginning of the 21st century, the interest rate has hovered below or barely above the zero level. Despite all this, inflation still remains far from the target, to the BOJ’s despair.

Conclusion

No other bank in the developed world has faced such difficult economic conditions as Japan has in the last couple of decades. Deflation constantly gripped the economy, affecting the bottom line.

In the meantime, the actions undertaken by the Bank of Japan are viewed as experimental by most other central banks in the developed countries. At first, after the QE programs were running in Japan and the United States, many central bank watchers, traders, and investors argued that this would end in tears. So far, though, both the BOJ and the Fed have been proven right, as the United States economy bounced and Japan remains afloat.

When the BOJ moved the interest rate level below zero for the first time, it was viewed as the pioneer of Negative Interest Rate Policy (NIRP). Many doubters shook their heads in disapproval.

Fast forward a few years, and NIRP is a reality in the Eurozone, Switzerland, some Nordic countries, and in other parts of the world. Today, the same voices that disapproved of the BOJ’s move are calling for the Fed to turn to NIRP.

To sum up, the BOJ was forced to become one of the most closely watched central banks in the world. Its inability to fight deflation despite tremendous efforts is a lesson for other central banks facing similar conditions.